.png)

As an advisor, I try to pay special attention to the questions that I hear repeatedly. Lately, one of those questions has been:

"Where should I put my money when the market is at all-time highs?"

At the time of this writing, the S&P 500 has hit a fresh market high for the past 4 days in a row.

I can hear the worry behind the question. You're thinking that what goes up must come down, right? And we've all been told to buy low and sell high.

But when I look at the actual data on long-term investing, I'm not convinced that timing the market based on current levels makes much sense for retirement planning.

It’s my (professional) opinion that of all the things we can not control throughout retirement, this fear does not have to be one of them. So hopefully this helps you too. Let’s dive in.

Here's what happens when you get stuck on this question. Your brain freezes up. Says "NO" to everything. Sometimes that works in your favor (you leave your 401k alone). Other times, you start hoarding cash and waiting for some mythical "coast is clear" signal that never comes.

The problem gets worse when you think you can outsmart the market with whatever economic headlines are grabbing attention this week.

Markets at all-time highs, unemployment numbers, interest rate changes, new trade policies. You start connecting dots that may not actually connect.

Let me share some data that might surprise you. Morningstar runs an annual study called "Mind The Gap" that tracks how individual investors perform compared to the funds they're actually invested in. If you’re like me, you may need to read that last sentence again.

How is that possible?

For the 10 years ending December 31, 2024, the average dollar invested in US mutual funds and ETFs earned 7.0% per year. That sounds decent until you realize the funds themselves returned 8.2% annually over the same period.

That's a 1.2% gap every year. Every single year.

It comes down to one thing: timing. People bought and sold at exactly the wrong moments. In other words, investors didn’t hold the investment for the full time period in hopes that they could achieve higher performance by dancing around market dips.

But what about those all-time highs specifically?

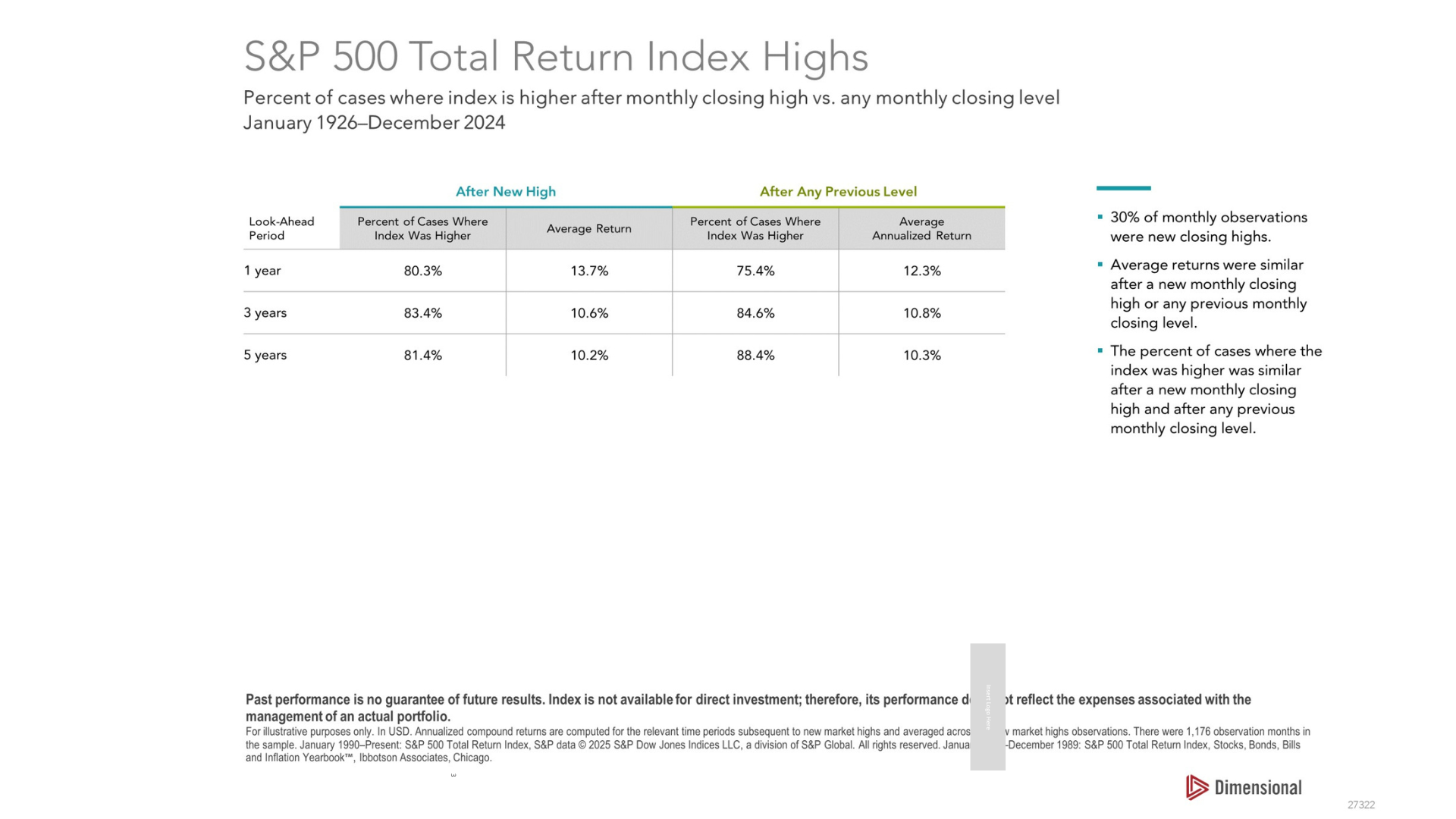

Research from Dimensional Funds looked at this question using data from January 1926 to December 2024. When the S&P 500 hit an all-time high, the market averaged 10.2% annually over the following five years. Markets were higher 81% of the time.

Compare that to investing at any random previous level: 10.3% average returns with markets higher 88% of the time. The difference is marginal.

Both scenarios give you strong odds of success if you have time on your side.

So instead of trying to find the perfect entry point, you can work with the data we already have. Markets tend to go up over time, regardless of whether they're at record levels when you start.

But I know what you're thinking. You’ve heard this before—play the long game. But what if you're retiring soon? What if you need this money in the next few years?

This is a legitimate concern.

This is called ‘sequence of return’ risk. Over the 30-35 years of returns you may get during retirement, what if the first year is a big downturn? Or what if there are several years of declining markets during this pivotal timeframe?

You can still maintain that long-term view, but only if you build your portfolio correctly. I structure retirement portfolios with several years of distributions sitting in cash, followed by another 3-5 years in less volatile assets like bonds. The money you won't need for 7-10+ years can ride out market bumps because you're giving it time to recover.

You never want to sell your stock investments during market pressure. Never.

That's when the real damage happens to retirement accounts. Not only is the portfolio declining, but you’re taking money out at the same time.

This risk can be controlled and the magnitude mitigated with a properly structured balance of asset classes.

This is why I focus so much on proper allocation across cash, bonds, and stocks. Each piece of your portfolio has a job to do.

Cash is your insurance policy when markets drop.

Bonds bridge the gap between your immediate needs and long-term growth.

Stocks handle the heavy lifting for money you won't touch for years.

Simple. But effective.

When my clients understand this structure, they don't panic during market stress. They know they have breathing room built in. This concept can be visualized nicely as well which is always helpful when applying financial concepts.

Here's what you can do right now to see where you stand. But this exercise only matters if you're in or nearing retirement. If you've got 10+ years before you retire, the data supports letting capital markets work for you regardless of market levels.

But, if you do find yourself with retirement on the horizon, look at your cash and near-cash investments (money market accounts, high-yield savings, short-term CDs). Figure out how many months of retirement expenses you could cover with just these liquid assets.

Let's say you need $10,000 a month to live comfortably in retirement, but $5,000 comes from Social Security and pensions. Your portfolio needs to provide the other $5,000, or $60,000 per year. In this case, you'd want roughly $120,000 in liquid cash assets to cover two years of distributions.

This exercise tells you whether you have enough of a buffer to let your long-term investments do their job, regardless of what the market does in the short run. And that buffer gives you the confidence to stay invested even when headlines make you nervous.

No more timing, no more guessing “when” to take advantage of the market.

When you can handle market volatility without making fear-based decisions, you put time back on your side.

Financial Advisor

Financial planning & investment management services for families & businesses

📍405 E Chocolate Ave, Suite 101 A, Hershey, PA 17033

Serving clients virtually nationwide