.png)

When it comes to Social Security, most lawyers I meet want a simple answer: "Should I take it at 62 or wait?" While I wish there was a one-size fits all response, the better question to ask may be:

"How does this decision fit into my complete retirement picture?"

Here's what happens when you claim:

At 62: You get about 70% of your full benefit

At full retirement age (66-67): You get 100%

At 70: You get 132% of your full benefit via delayed credits

Most people stop there. They see the big increase from claiming at 70 versus 62 and think that settles it. But that's just the starting point of the analysis.

Let me tell you about Tom, a solo practitioner approaching retirement. His full Social Security benefit at 67 would be $3,200 monthly. The question wasn't just "when should he claim?" but "how does this decision integrate with his overall retirement strategy?"

Here's how we approached it:

Step 1: Analyzed his complete financial picture – retirement accounts, other income sources, projected expenses, and tax situation.

Step 2: Modeled different claiming scenarios against his specific circumstances. What if he claimed at 62? At 67? At 70?

Step 3: Considered factors beyond just the benefit amount – his health outlook, his wife's survivor benefit needs, his tax bracket implications.

Step 4: Integrated the Social Security decision with his overall withdrawal strategy to optimize lifetime income.

For Tom's specific situation, delaying until 70 while using other retirement assets as a bridge made tremendous sense. But the key insight isn't that delaying is always right – it's that we used systematic analysis to reach that conclusion.

I've worked through this framework countless times where the best decision pointed us in a different direction. Sometimes claiming at full retirement age makes the most sense. Sometimes even claiming early is the right call.

The difference isn't luck or guesswork – it's having a comprehensive approach that accounts for:

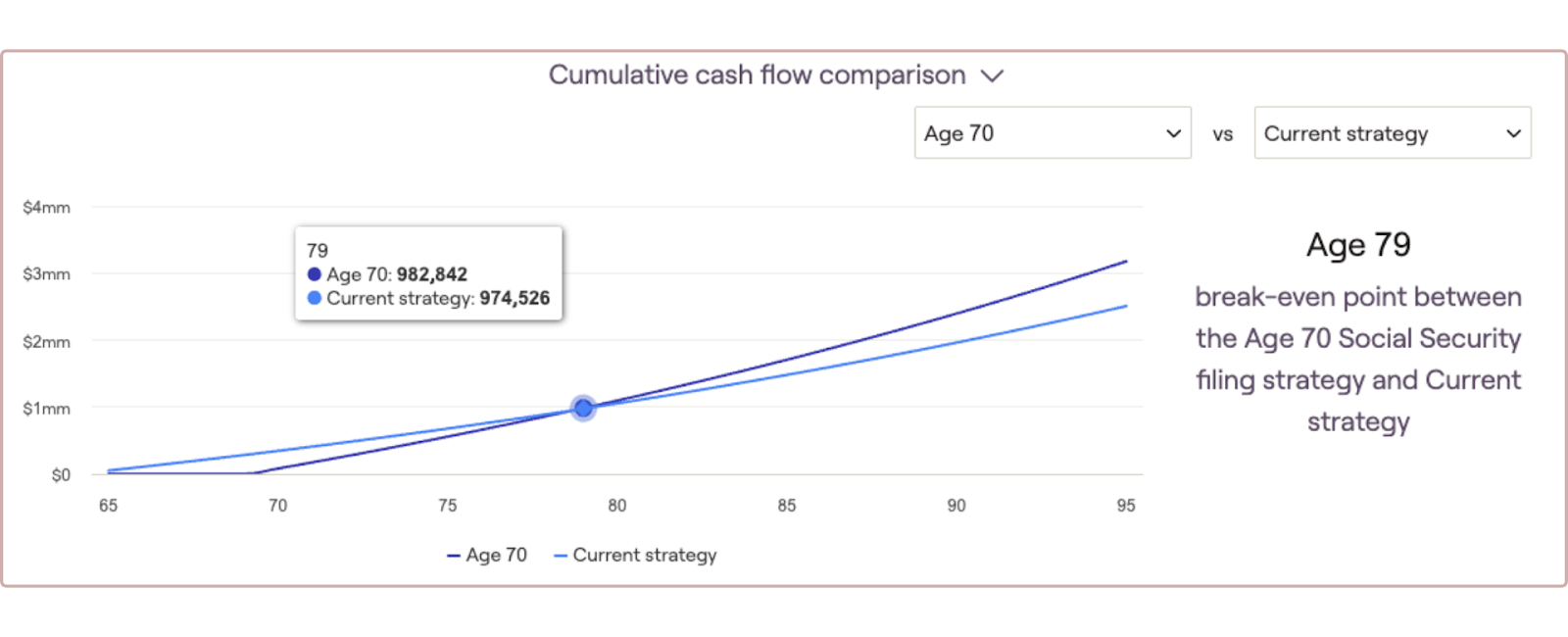

Here’s a different scenario where we ran a “Break-even” analysis. Here’s how it works:

We’ve already established that delaying your social security can result in a larger benefits check. However, for those that collect earlier—Let’s use 65 as an example—are collecting benefits for 5 years before the attorney who decides to delay until age 70. This begs the question:

How long does it take for the lawyer who delays claiming Social Security to catch up in “Total benefits paid” to the early collector?

The graph below shows total Social Security benefits received at various ages. Benefits at Age 65 were about $2,780 per month for Spouse #1 and about $1,390 for Spouse #2. Delaying until age 70 increases these benefits to $4,501 and $2,250 respectively.

And in this case, the break-even—The age in which total benefits claimed by delaying benefits to Age 70surpasses collecting at Age 65— is…. Age 79.

Again—Not that this is right or wrong—Just an example of how your various benefits work together in retirement. The timing around your decision to collect Social Security benefits should incorporate these other factors.

The question isn't whether you can afford to delay Social Security – it's whether you're making this decision based on your complete financial picture or just following generic advice.

This choice will impact you for decades. It deserves more than a gut feeling or conventional wisdom.

Are you analyzing your Social Security timing based on your complete financial situation, or are you planning to make this decision in isolation?

Financial Advisor

Financial planning & investment management services for families & businesses

📍405 E Chocolate Ave, Suite 101 A, Hershey, PA 17033

Serving clients virtually nationwide