.png)

You've done the math. You've calculated your retirement needs. You've figured out your portfolio target. But there's one more piece of the puzzle that could change everything about your retirement planning: flexibility.

And I'm not talking about yoga classes (though those might be nice too). I'm talking about the willingness to adjust your retirement spending based on how your investments perform—and why this single mindset shift could be the difference between retiring comfortably and working until you're 70.

Research shows that most retirees don't increase their spending with inflation every year anyway. Instead, spending follows more of a "smile" pattern: higher in early active years, lower in the middle period, then rising again with healthcare costs in later years.

I find this true in practice. Even with the last few years of high inflation, most of my retirees have taken inflationary bumps to their withdrawals, but much lower than the actual rate of inflation.

Think about it logically. You're not going to be taking expensive adventure trips when you're 85. You're probably not going to be buying new cars every few years. Your entertainment expenses might shift from expensive dinners out to more time reading at home.

A flexible spending strategy means adjusting your withdrawals based on how your investments perform. Being willing to reduce spending by just 5-10% during major market downturns can let you start with a higher withdrawal rate and still make your money last.

For attorneys used to unpredictable income, this flexibility comes naturally. You've dealt with lean months and windfall months throughout your career. Retirement doesn't have to be different.

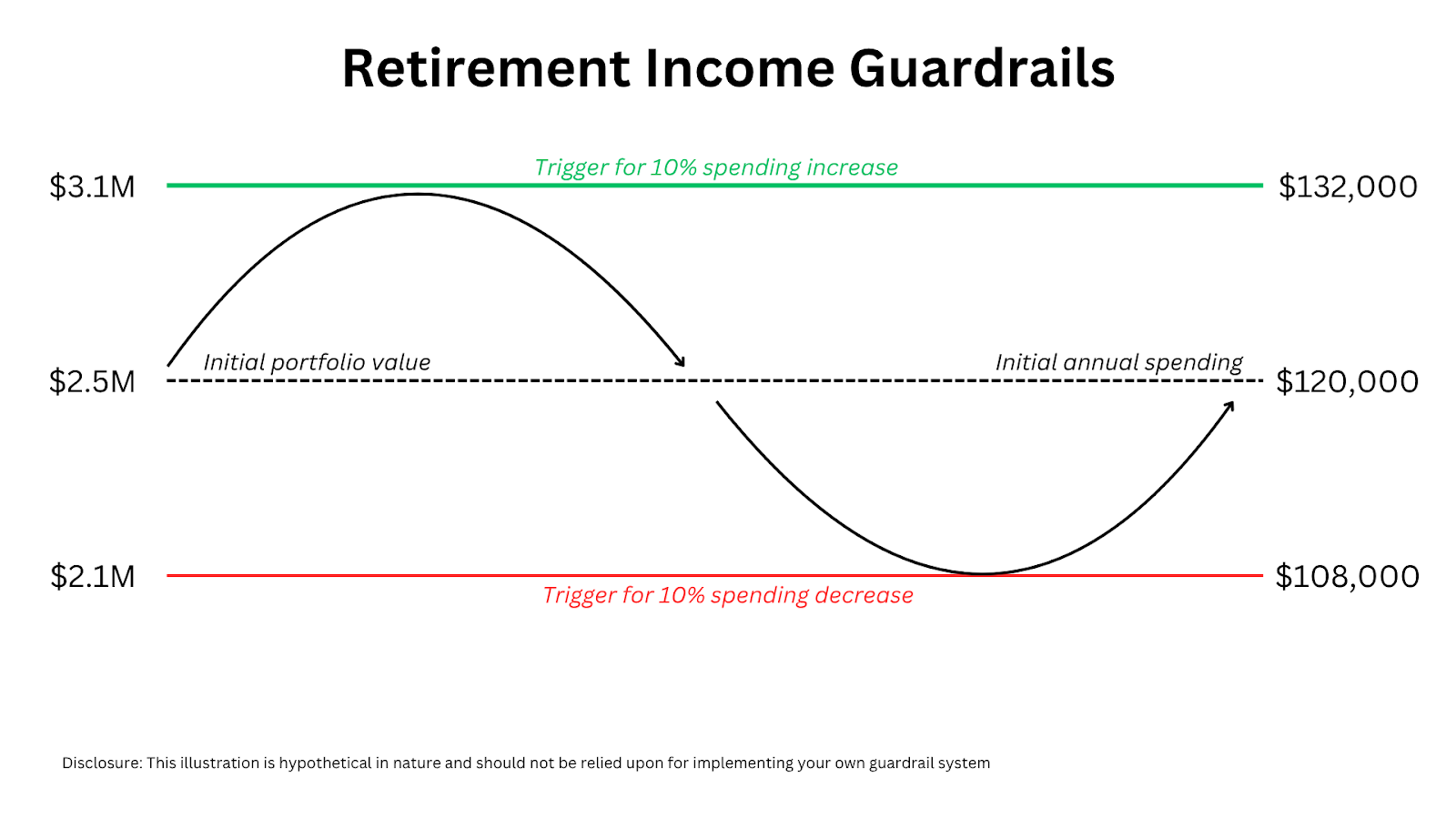

Let's get super clear with how this works in practice. Say you retire with $2.5 million and plan to withdraw $120,000 annually (4.8% initial rate). Here's how guardrails might work:

If our initial draw rate increases by 20% (4.8% x 120% = 5.76%) due to a reduction in portfolio value (or unplanned portfolio withdrawals), this will be our trigger for a 10% decrease in spending.

Conversely, if our initial draw rate decreases by 20% (4.8% x 80% = 3.84%) due to favorable market conditions or additional contributions to the portfolio, this will be our trigger for a 10% increase in spending.

To give an example with real numbers:

Note: I used some rounding in these examples to keep the numbers clean, but the overall principal is what’s most important here.

Notice these shifts are not dramatic changes. You're making small adjustments that keep your retirement sustainable without derailing your lifestyle.

Now this is just one example of what is called a “Withdrawal Rate Guardrail”. In practice, we can apply guardrails in alternative ways, including “Risk-Based Guardrails” that use a Monte Carlo score instead of a withdrawal rate. In doing so, we can better account for your mortgage dropping off in year 7, or a decrease in portfolio withdrawals after Social Security income kicks in.

In other words, you wouldn’t continue to withdraw your $4,000 mortgage payment after it’s paid off. Therefore, your withdrawal rate would change, but your Probability of Success would not because that’s how we’ve modeled your plan in the first place.

The take-home point here is that you don't have to get your retirement calculation perfect if you're willing to make adjustments throughout retirement. This is incredibly freeing for attorneys who tend to want everything mapped out precisely.

The traditional retirement planning approach says: "Figure out exactly what you'll spend for 30 years, then save enough to support that exact amount." But life doesn't work that way.

Maybe you'll travel more in your early retirement years. Maybe you'll spend less when you're older. Maybe you'll have unexpected expenses. Maybe you'll inherit money. Maybe the market will do better than expected.

But what about that nightmare scenario where the market crashes right when you retire? This is called sequence of returns risk, and it's a real concern.

The solution isn't to save an extra $500,000 just in case. It's to build flexibility into your plan. Maybe you delay that kitchen renovation for a year. Maybe you take a smaller vacation. Maybe you reduce your charitable giving temporarily.

These aren't life-altering changes. They're small adjustments that could extend your portfolio's lifespan significantly.

Here's what I've learned after years of helping people with retirement planning: confidence matters more than perfection.

The attorney who has $2.3 million saved and is comfortable adjusting their spending will likely have a better retirement than the one who has $3 million saved but is terrified of spending any of it.

Why? Because retirement isn't just about having enough money. It's about having enough confidence to actually enjoy the money you've saved.

You already have skills that make you perfect for this approach. You're used to:

These are exactly the skills that make dynamic retirement planning work.

Understanding your retirement costs isn't about creating a perfect budget that you'll follow for 30 years. It's about getting clear on what you actually need so you can make informed decisions about when and how to retire—and when to adjust along the way.

The math might seem daunting at first, but remember that small changes in your expenses can add years to how long your money lasts. And with some strategic planning around taxes, work expenses, and flexible spending, you might find that retirement is closer than you think.

The goal isn't perfection. It's confidence that you can maintain your lifestyle without the pressure of billable hours and court deadlines.

Start building that confidence today by getting clear on your current spending. Then we can worry about fine-tuning the details—and building in the flexibility that will make it all work.

Financial Advisor

Financial planning & investment management services for families & businesses

📍405 E Chocolate Ave, Suite 101 A, Hershey, PA 17033

Serving clients virtually nationwide