.png)

Last week I walked through Phase 1 of the Attorney Transition Plan: getting clear on why you're leaving, and where you actually stand financially.

This week is Phase 2: Design. This is where the planning gets real.

Phase 1 was about assembling an honest picture. Phase 2 is about doing something useful with it.

Most attorneys I work with have looked at account balances. Maybe run a calculator online. But they've never sat down and watched what happens to their taxes when you move a retirement date by five years.

That's what Design is. And a recent client is the best way to show you what I mean.

A law firm partner came to me last year — 60 years old, $2.2 million saved, and another $1 million owed to him as an equity partner. Had his number in his head: 70. That was the earliest he thought he could walk away.

But he'd never modeled the transition. He'd been planning around a retirement date without ever looking at what happens between the date he leaves and the date he starts spending down his accounts.

His buyout terms were standard. $1 million in equity, paid over five years, no interest. $200,000 a year.

He'd always thought of the buyout as a bonus on top of his retirement savings. What he hadn't done was look at those payments as what they actually are: income. $200,000 a year, for five years, arriving whether he worked or not.

That changed everything.

Most attorneys think about a buyout as a one-time event. But the payments stretch out over five or ten years. That changes everything about what follows.

His personal expenses were about $180,000 a year. The buyout more than covered that.

So he could leave his retirement accounts completely alone from 65 to 70. No withdrawals. No taxable distributions. Five years of uninterrupted compounding.

And every year he didn't pull from those accounts was a year he wasn't stacking buyout income on top of retirement account withdrawals in the same tax return.

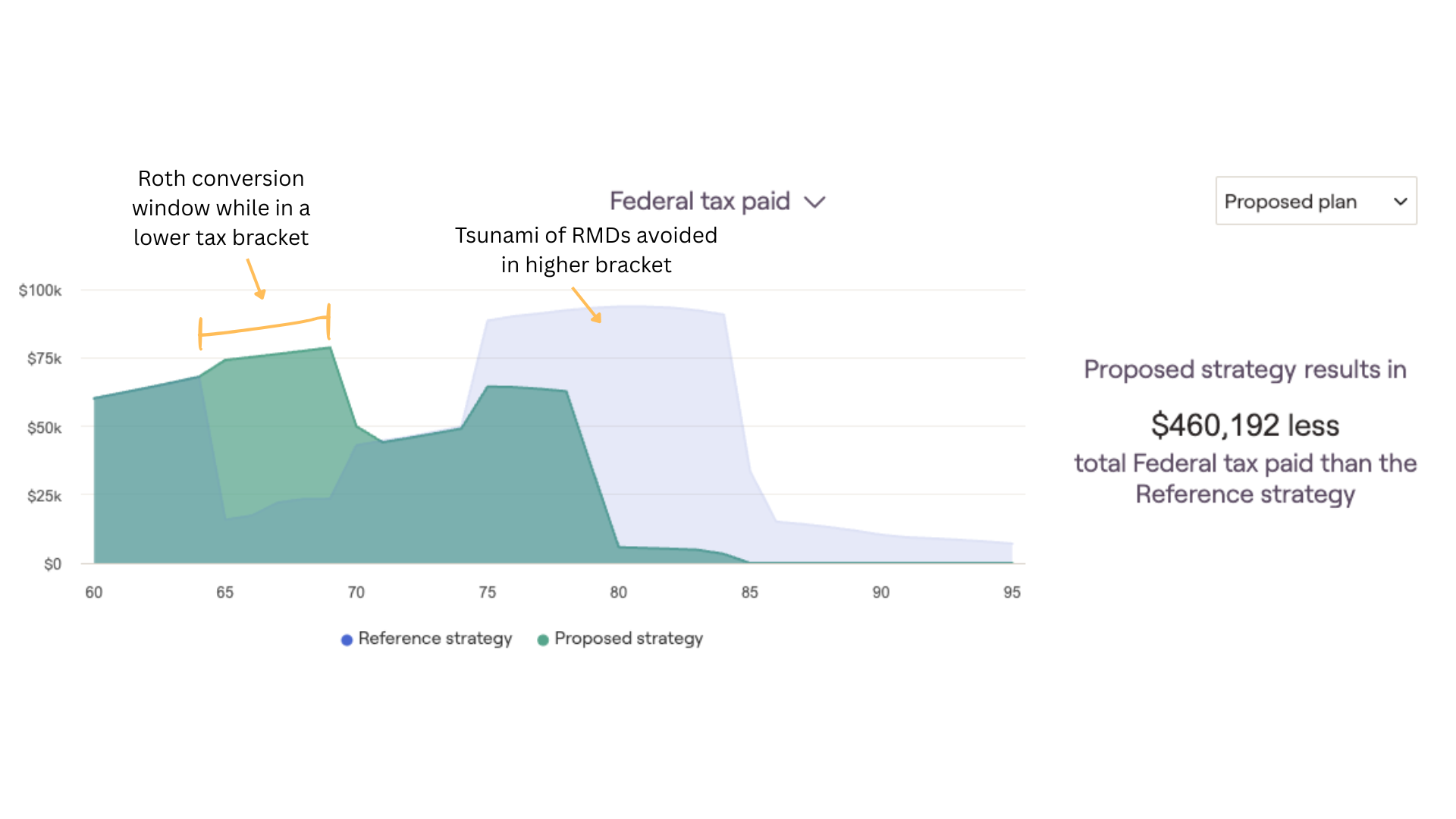

When we ran the side-by-side (retire at 65 with the buyout funding his lifestyle, versus working until 70 and taking everything later) the plan projected over $400,000 in tax savings. That's not a rounding error.

Retiring at 70 seemed like the safe move. More years of income. A bigger balance at the finish line.

But when we looked at the tax picture, it told a different story.

At 70, his buyout payments would land at the same time as Social Security. And required minimum distributions would soon follow. All of that income hitting in the same years, pushing him into higher brackets with zero room to maneuver.

At 65, the sequencing was completely different. Buyout income fills years 65 through 70. Social Security gets delayed to 70, when it's worth more.

And remember that $400,000 in tax savings? Here's how. Those five lower-income years between 65 and 70 create a wide-open window for Roth conversions, moving money from pre-tax accounts into a Roth at a fraction of the tax cost he'd pay later.

He didn't need to work five more years. He needed a plan that put the pieces in the right order.

A quick note: this example is for educational purposes only and isn't investment advice. There are a number of other assumptions, variables, and terms that go into a plan like this. Every attorney's situation is different, and yours needs to be evaluated individually. The point here is to show what becomes possible when the pieces are modeled together.

A retirement calculator tells you if you have enough money. Design tells you what to do with it, and when.

Move your retirement date by five years and your buyout timeline shifts with it. That changes when Roth conversions make sense, when Social Security kicks in, and when you start pulling from your portfolio. One variable moves and everything else moves with it.

That's why a coordinated, tax-aware strategy looks so different from a collection of accounts with a target withdrawal rate.

By the end of Phase 2, you should know what changes if you leave at 62 versus 65 versus 68. Not a guess. Actual projections with income, taxes, and spending mapped year by year.

You should see how your buyout or practice sale terms ripple through the rest of the plan. Where the tax windows open. And what order to draw from your income sources, because the sequence matters more than the totals.

Phase 3 is where the plan produces an answer. Not another "almost ready" — an actual go or no-go, with the stress testing to back it up. That's next week.

If anything here sounds familiar, if you've been running the mental math but haven't seen it modeled, I'd like to hear where you are. Reply and tell me. I read every one.

— David

Financial Advisor

Financial planning & investment management services for families & businesses

📍405 E Chocolate Ave, Suite 101 A, Hershey, PA 17033

Serving clients virtually nationwide