.png)

You saved well. For decades. Every year, you maxed out your 401(k), funded your traditional IRA, and watched the balance grow.

And now you're approaching retirement with a million dollars (or more) locked inside tax-deferred accounts.

Congratulations. You did exactly what you were told to do.

Oh, just one more thing—the IRS hasn't forgotten about that money. They've just been patient.

Before we get into the strategy, let me level-set on a few terms.

A Roth conversion is when you move money from a traditional IRA or 401(k) into a Roth IRA. You pay income tax on the amount you convert in the year you do it. After that, the money grows tax-free. And when you pull it out in retirement, you owe nothing.

A Required Minimum Distribution (RMD) is exactly what it sounds like. Starting at age 73 for most, the IRS requires you to withdraw a minimum amount from your tax-deferred accounts each year. You don't get a choice. And every dollar comes out as taxable income.

With those definitions out of the way, let me show you why this matters so much for lawyers.

Most lawyers I talk to have done a tremendous job accumulating wealth inside tax-deferred accounts. 401(k)s. Traditional IRAs. SEP IRAs if you were a solo practitioner.

The problem here is that every dollar that comes out is taxed as ordinary income. All of it.

So let's say you're 68, retired, and you need $150,000 for the year. Maybe it's your normal living expenses. Maybe your daughter is getting married. Maybe you want to buy a place in Scottsdale.

If the bulk of your savings is sitting in a traditional IRA, you're pulling that $150,000 out and stacking it on top of your Social Security income. Suddenly you're in the 24% bracket. Or the 32% bracket.

And it gets worse. That spike in income can trigger taxes on up to 85% of your Social Security benefits. If you have investments in a taxable brokerage account, your capital gains rate is tied to your adjusted gross income. Push that AGI high enough and your 15% capital gains rate jumps to 20%.

One big distribution creates a ripple effect across your entire tax picture.

A Roth conversion done in the right years, at the right amounts, slowly builds a pool of tax-free money you can tap without any of those consequences. You're creating liquidity that doesn't show up on your tax return.

Now here's where it really gets interesting for lawyers who retire before 73.

Let's say you leave the firm at 65. You've got a pension, some Social Security, and maybe some rental income. Your taxable income drops significantly. You're in a lower bracket than you've been in for 30 years.

Most lawyers I see in this situation do one of two things. They either take minimal IRA distributions to cover expenses, or they don't touch the IRA at all. They think, "I want this money to last. I'll let it keep growing."

Makes sense on the surface. But that IRA doesn't just sit there quietly. It keeps growing. And growing. And at age 73, the IRS shows up and says, "Time to start withdrawing."

Your first RMD might be manageable. But by 78, 80, 83, those required distributions are getting larger every year because the IRS formula forces you to take out a bigger percentage as you age.

Now you've got a tsunami of taxable income you can't avoid. And the cascading effects kick in again: taxes on Social Security, higher capital gains rates, and (as we've talked about in past editions) IRMAA surcharges on your Medicare premiums. IRMAA looks back two years at your income, so a big RMD at 75 means higher Medicare costs at 77.

That's the tax bomb. And it was completely avoidable.

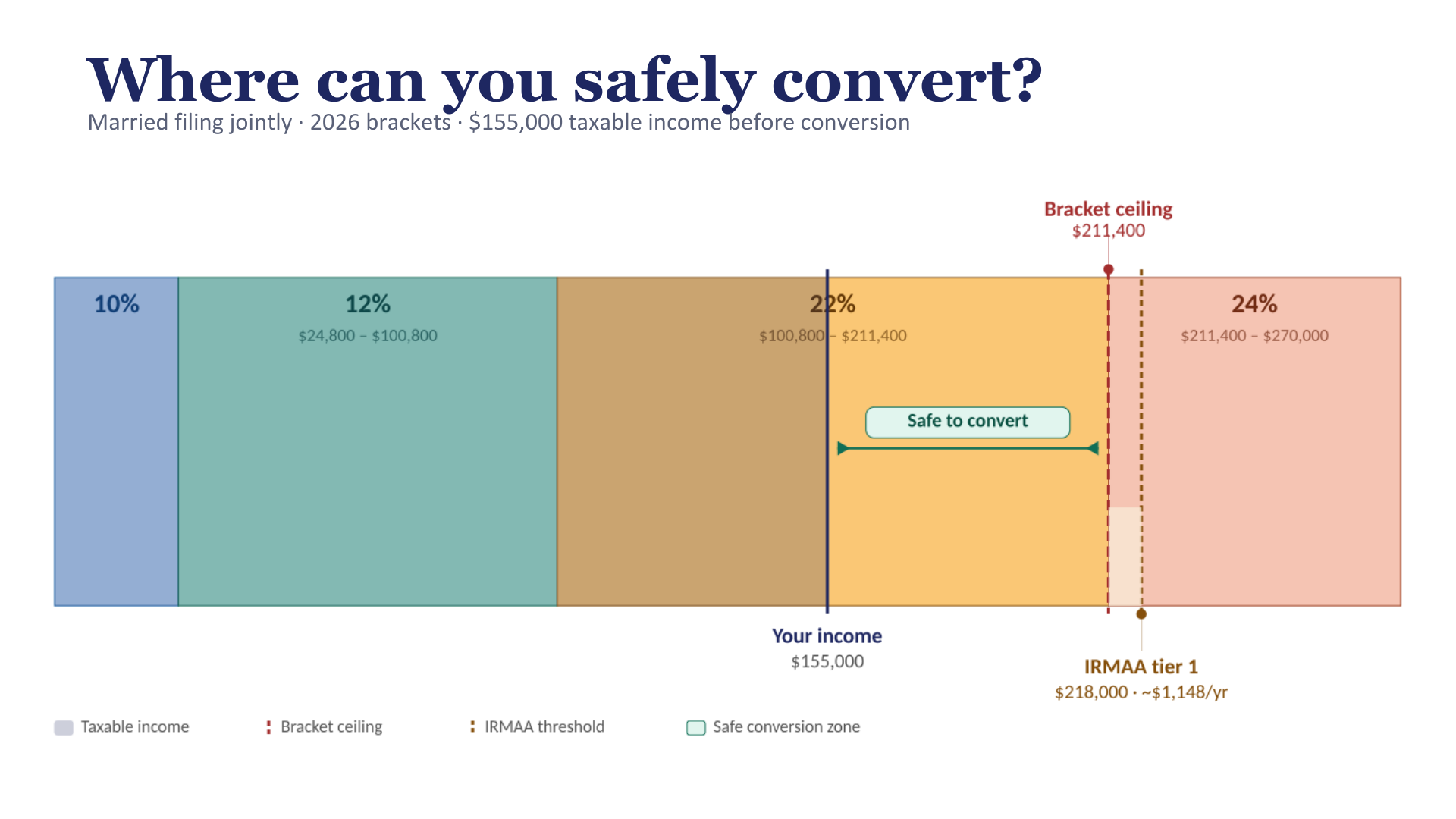

The years between retirement and age 73 are some of the most valuable tax planning years of your life. Your income is lower. Your bracket is lower. And you have the opportunity to strategically convert portions of your traditional IRA into a Roth, paying taxes at today's lower rate instead of tomorrow's higher one.

You don’t have to convert the whole balance at once. That would defeat the purpose. We're talking about doing the math each year and filling up your current tax bracket with conversions. Converting just enough to stay below the next bracket threshold.

Here’s what this looks like visually:

Done right over 5 to 8 years, you can meaningfully reduce those future RMDs, create a flexible source of tax-free income, and take real control over what your tax picture looks like for the rest of your life.

This is the kind of planning that doesn't happen by accident. It takes projections, coordination with your CPA, and a strategy that adapts each year based on your actual numbers.

If you've been letting your IRA grow untouched since you retired, it might be worth asking: what's that account going to look like at 73? And what's the IRS going to demand you take out?

The answer might surprise you. And the time to act is before the clock runs out.

Financial Advisor

Financial planning & investment management services for families & businesses

📍405 E Chocolate Ave, Suite 101 A, Hershey, PA 17033

Serving clients virtually nationwide