.png)

Over the past few weeks, we've talked about why the traditional retirement model fails lawyers. We've explored transition pathways that help you retire to something meaningful, not just from your practice. Most of that discussion focused on the emotional wins of reframing retirement.

If you missed those editions, I'd encourage you to check the archives.

Today I want to talk about the financial benefits of a clear transition plan. These benefits include a more fulfilling retirement and real protection for your portfolio's longevity.

Most lawyers who retire need their assets to last 30 years. Some need more, some less. That objective brings all kinds of risks: sequence of return risk, overspending risk, underspending risk, longevity risk. The list goes on.

But there's one strategy that eases pressure on your portfolio during those critical early retirement years. And it makes a lasting impact across your entire time horizon.

Here it is: A part-time income, even a small one compared to your lawyer wages, can dramatically improve your retirement outlook.

Many lawyers underestimate this impact. And it fits perfectly with what we've discussed about retiring to something meaningful.

Let me show you with a real example (names changed, of course).

Caleb has a 401(k) worth $1,025,000 and a Roth IRA at $200,000. Rachel has a Roth IRA worth $225,000 and a rollover IRA at $250,000. They own a joint brokerage account valued at $300,000. Their home is worth $750,000, and they just made their final mortgage payment.

They'll both collect Social Security starting at 67. Rachel also has a small pension paying $30,000 annually.

Their goal? Retire this year at 65. They estimate they need $12,000 monthly for core living expenses, plus healthcare costs and taxes on portfolio withdrawals.

When we looked at their first-year cashflow, we found a problem. Rachel's $30,000 pension was their only income (they weren't taking Social Security yet). Expenses and taxes totaled $180,000. That created an "income gap" of $150,000.

They'd need to pull $150,000 from investments in year one just to cover their needs.

In year three, when Social Security kicked in, that withdrawal dropped to about $90,000. But the damage was already done. The first years of retirement are pivotal, and this plan put enormous pressure on their portfolio right out of the gate.

When we ran the analysis, the Justice family had what I'd call an "iffy" plan at best. Their assets dropped substantially throughout retirement, with a steep fall near the end when we factored in potential long-term care costs.

Technically, the straight-line analysis showed some funds remaining at the end. A straight-line analysis assumes consistent investment returns throughout retirement.

The problem? We know with certainty that returns won't be consistent. Market returns vary wildly. Even though the S&P 500's average return looks stable, it rarely delivers that exact number in any given year. For example, since 1926, the S&P 500 has returned an average of over 10% per year. However, it’s only earned its average in 6 of the past 93 calendar years.

Sequence of returns matters enormously. When we ran the Monte Carlo simulation with 1,000 different return combinations, only 50% showed a successful plan.

Not exactly the confidence Caleb and Rachel were hoping for.

"Guess I'll just work another five years," Caleb said.

He was right. Five more years made the plan look rosy. It certainly beat the other option: cutting spending dramatically.

We discovered that both Caleb and Rachel felt nervous about quitting work cold turkey.

Caleb had been wanting to start a consulting business. He'd built a prominent name in the community and wanted to explore passions that actually inspired him. He'd already written a business plan but felt too apprehensive about leaving law.

His projected consulting earnings would be much less than his lawyer income. That bothered him.

Until he realized this might be the key to "retiring" on his terms. Transitioning into work he genuinely enjoyed. And as it turned out, this additional income changed everything.

At 65, Caleb projected earning about $60,000 annually from consulting. He was comfortable planning for seven years (though he might continue to 80 if he enjoyed it).

Rachel found a part-time role with her favorite nonprofit, earning $10,000 per year while volunteering the rest of her time.

Peanuts, right? You'd be surprised.

Combined, that's $70,000 for the first seven years. While I'm not a fan of the 4% rule generally, I do use it for quick calculations. Earning $70,000 doing something you love is like borrowing a $1.75 million portfolio for those years.

It takes pressure off those large early withdrawals, which creates a cascading effect. More stable income softens sequence of return risk because fewer assets get withdrawn early on.

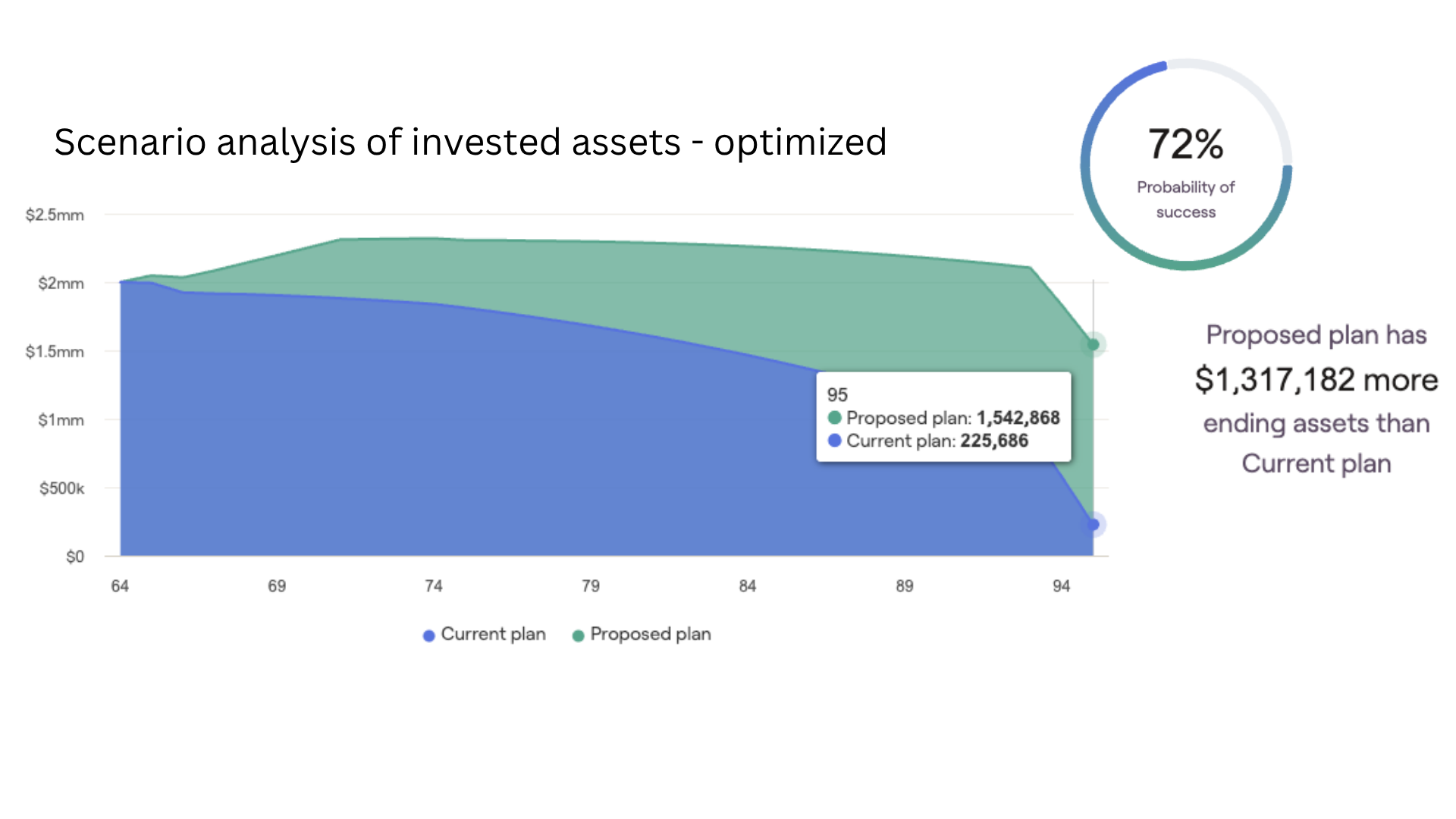

The comparison was substantial. The assets that stayed invested generated an additional $900,000 over the plan's time horizon. The Monte Carlo score jumped from 50% to 65%, almost reaching our 70% target zone.

This let us adjust their travel budget more realistically, modeling it through the first 10 years instead of to age 95. That makes sense when you consider health and energy levels as retirement progresses.

The final result? The plan generated more than $1.3 million compared to our base case, with a 72% probability of success. Here’s the before, in blue, and the after highlighted in green:

The most meaningful part? Caleb and Rachel could retire and feel excited about this next chapter. No loss of mental sharpness. More purpose. A much-needed change for both of them.

Sometimes the best financial strategy is also the most fulfilling one.

If you're approaching retirement, don't overlook what a strong transition plan can do for you. The emotional benefits are real: more purpose, continued engagement, excitement about what's next. But the financial benefits are just as powerful. A plan that lets you retire to something meaningful doesn't just create a more fulfilling retirement. It creates a more financially sound one too.

Financial Advisor

Financial planning & investment management services for families & businesses

📍405 E Chocolate Ave, Suite 101 A, Hershey, PA 17033

Serving clients virtually nationwide