.png)

About six months back, I had a "Learn More" call with an attorney who'd done everything right. He'd maxed out his 401(k) for decades, stuffed money into traditional IRAs, and built substantial wealth while slashing his tax bills year after year.

His concern wasn't having "enough" for retirement – it was figuring out how to unwind his mostly tax-deferred portfolio without getting hammered by taxes.

"I followed all the conventional wisdom," he told me. "But now I'm looking at this massive tax-deferred balance, and every dollar I pull out becomes taxable income."

Could be worse, right? But he needed flexibility.

What if he wanted to buy that retirement home? Help a kid with a down payment? Handle an unexpected expense? Taking large chunks from his 401(k) or traditional IRA would create a tax nightmare and push his other income sources into higher brackets.

Fortunately, he had some money in taxable accounts and Roth IRAs. Plus, he was charitably inclined, which opened up additional strategies.

But his situation perfectly illustrates the challenge I see constantly when talking with lawyers approaching retirement.

You've probably walked the same path. Max out that 401(k), follow expert advice to the letter, and watch those tax-deferred accounts grow. Smart move – it likely saved you thousands each year during your earning years.

But here's what that conventional wisdom creates: a retirement distribution challenge.

Every dollar you pull from those traditional accounts becomes taxable income. Need an extra $250,000 for that retirement home down payment? Yikes. Taking it from your 401(k) costs you $250K plus taxes and pushes your pension and Social Security into higher brackets too.

It feels like being penalized for all the tax-smart accumulation in the first place, doesn’t it?

Having substantial tax-deferred savings is still a massive win. You saved taxes for years and built real wealth. And the good news is that having mostly tax-deferred assets does present some real planning opportunities to give you more flexibility in retirement.

And today, we’ll take a look at some of the low-hanging fruit.

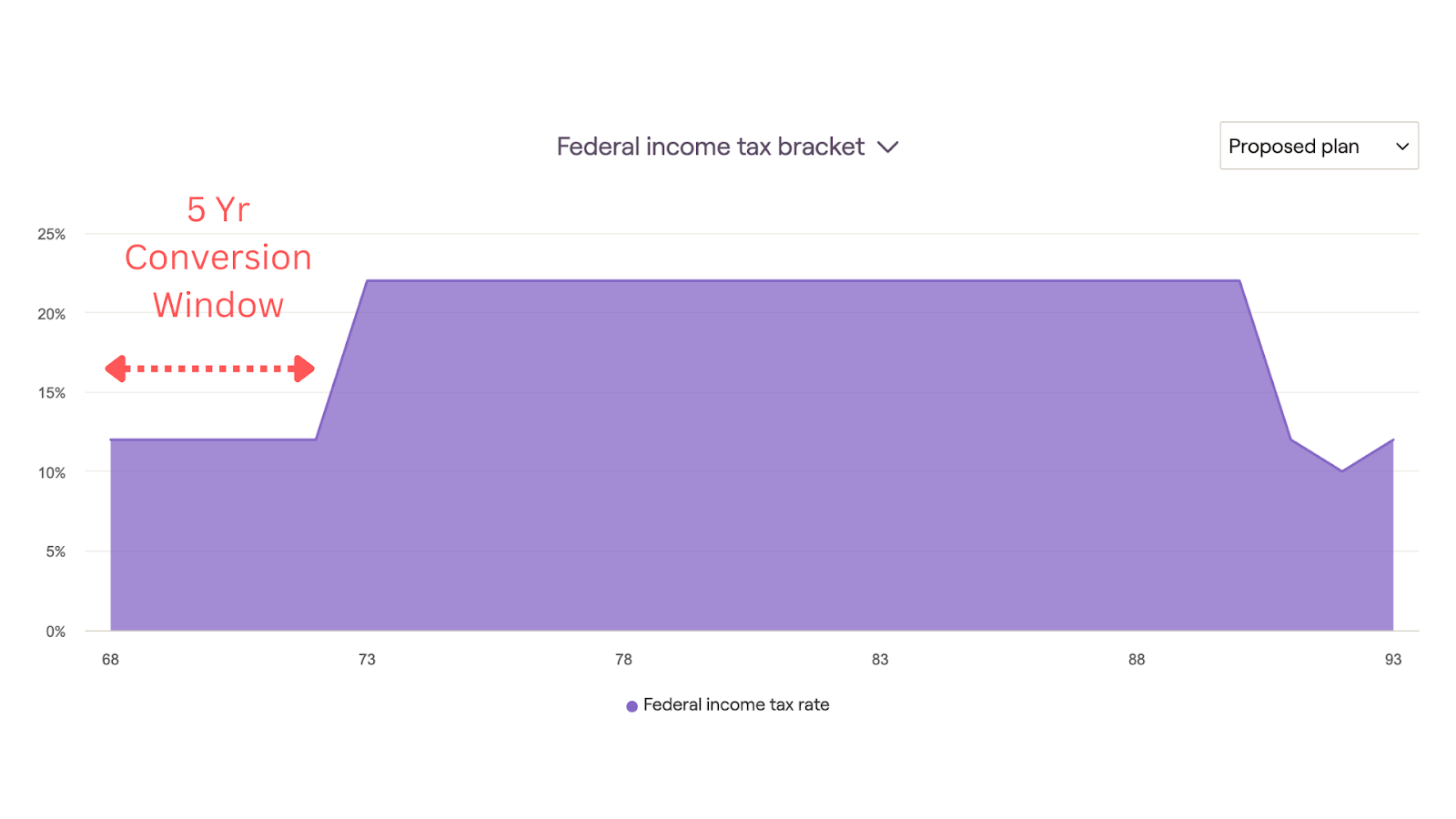

You'll likely face your highest tax rates right as required minimum distributions kick in at 73, especially if you’ve delayed Social Security claiming until age 70.

This creates a golden window for Roth conversions. Converting portions of your traditional IRA to Roth during lower-income years can make sense for some. The idea here is that you’re paying taxes at today's rates to create tax-free income later. It's like prepaying your taxes when the bill's smaller.

What’s interesting here is that this will most assuredly increase your tax exposure in the current year. But you have to zoom out and ask yourself:

Is the goal to pay less taxes in any one year? Or is it to lower taxes over my lifetime? And usually, it’s the latter.

If you're charitably minded and over 70½, QCDs are your friend. You can transfer up to $108,000 annually (per individual) directly from your IRA to qualified charities. How is this beneficial? It counts toward your RMD but doesn't show up as taxable income.

Notice I prefaced this with “If you’re charitably minded..”

In other words, using charitable giving solely to save on taxes can be disappointing — you’re still parting with the money. But if you’re already donating by writing a check or paying out of pocket, you might get a greater benefit by giving directly through a QCD.

Smart retirement income planning means getting super clear about when your taxes will be highest and lowest. Maybe that's the gap between early retirement and Social Security. Or perhaps managing income around Medicare premium thresholds.

Looking out for some of those lower income years may give you a chance to facilitate income to smooth out the tax bumps ahead.

Here’s an example from working through this recently with a client:

Here's where having multiple account types becomes crucial. Bad market year? Harvest losses in your taxable accounts while pulling income from Roth IRAs. Good market year? Let those taxable accounts ride while converting more traditional IRA dollars to Roth.

You get options when life throws curveballs.

Even small balances in different account types can make a huge difference. Growth assets work beautifully in Roth IRAs where appreciation grows tax-free forever. Meanwhile, inefficient investments like bonds and REITs make sense in traditional accounts where you're paying ordinary income rates anyway.

For example, you may have a 60% Stock and 40% Bond portfolio across a Traditional IRA, a Roth IRA, and a Taxable Brokerage Account. However, your Roth IRA may have 100% Growth Equities in it. This is because you’re expecting your volatile growth assets to appreciate most over time, so why not make them tax-free?

Think of it as putting the right tools in the right toolboxes. I created this visual to better illustrate:

The strategies I've outlined require some initial legwork and ongoing attention. But the tax savings over a 20-30 year retirement can be substantial – sometimes six figures or more.

If this is you–you've already proven you can build wealth. Now it's time to get strategic about keeping more of it.

These strategies focus on creating flexibility and options for whatever retirement throws your way.

You've got this. The foundation is solid. Now let's build the distribution strategy that matches your accumulation success.

Financial Advisor

Financial planning & investment management services for families & businesses

📍405 E Chocolate Ave, Suite 101 A, Hershey, PA 17033

Serving clients virtually nationwide