.png)

If you're a successful attorney approaching retirement, here's something your Medicare handbook won't tell you clearly enough: your Medicare premiums might be two or three times higher than the "standard" rate you’ve read about.

Welcome to IRMAA—the Income-Related Monthly Adjustment Amount. It's Medicare's way of saying, "You made good money during your career, so you're going to pay more for coverage."

For most lawyers, IRMAA surcharges are almost inevitable in early retirement. The question isn't whether you'll pay them, but how much—and whether you can strategically reduce them.

I’ve had a flurry of new subscribers to the newsletter after my most recent column over at Above The Law—which was all about Medicare. So I wanted to circle back on some of the specifics most relatable to the retiring lawyer. If you’re new here, welcome 👋.

And if you missed last week’s edition, it lays the foundation for choosing between Original Medicare and a Medicare Advantage plan. I’d encourage you to check that out if you missed it.

And now, let’s jump in to IRMAA planning:

Your 2026 Medicare premiums are based on your 2024 Modified Adjusted Gross Income from your tax return.

Read that again. There's a two-year lag between the income you earn and the Medicare premiums you pay.

This creates a unique problem for retiring lawyers. Your high-earning years as a practicing attorney directly affect your early retirement Medicare costs. You might retire in 2024 with your earnings dropping to zero, but in 2026 you're still paying IRMAA surcharges based on what you earned in 2024 while working.

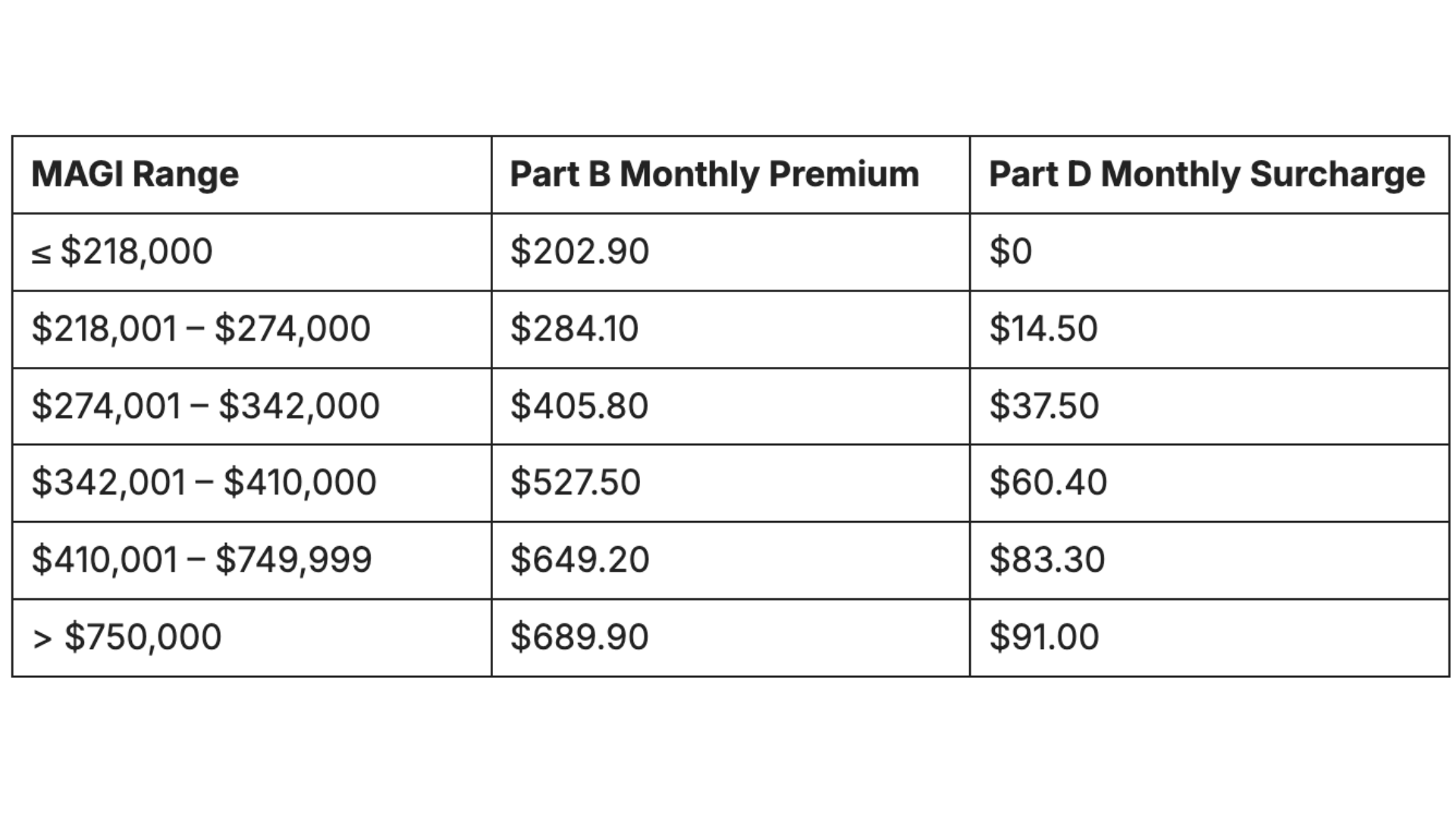

Let me show you what IRMAA looks like in 2026 for married couples filing jointly:

For single filers, these thresholds are roughly half.

Notice the jump from the standard $202.90 premium to $284.10 once you cross $218,000 in MAGI. That's an extra $974 annually per person. For a married couple, you're looking at an additional $1,948 per year just for crossing that first threshold.

And it gets steeper as you move up. A lawyer couple with $350,000 in MAGI pays $527.50 per person monthly for Part B alone—that's $12,660 annually versus the standard $4,870. We're talking nearly $8,000 more per year.

If you follow my work, you know I regularly write about strategic Roth conversions as a way to reduce lifetime taxes in tax-deferred accounts. Conversions can save you tens of thousands in taxes over retirement.

But, as it pertains to IRMAA, there’s a catch: Roth conversions count as income for IRMAA purposes.

And therein lies the planning dilemma. You might execute a $100,000 Roth conversion in 2024 that saves you $25,000 in lifetime taxes. But two years later, in 2026, that conversion income could push you into a higher IRMAA bracket, increasing your Medicare premiums by $2,000-$4,000 for that year.

This doesn’t mean you should throw roth conversions away.

It does mean you need to be thoughtful about timing and sizing your conversions, especially in the years immediately before and after Medicare enrollment.

The window between retirement and age 65 is often your best opportunity for larger Roth conversions. You're no longer earning W-2 income pushing you into high brackets, but you're not yet subject to IRMAA surcharges. This is when you can potentially convert larger amounts while staying below the higher IRMAA thresholds.

Once you're on Medicare, you'll want to model each year's conversion against the IRMAA brackets for two years later. Sometimes it makes sense to convert right up to an IRMAA threshold. Other times, you might deliberately stay below a threshold to avoid crossing into the next surcharge tier.

As you can see, these conversions require coordination among your tax planning, withdrawal strategy, and Medicare premium management.

There is good news in all of this: you can appeal your IRMAA determination if you've experienced a "life-changing event" that reduced your income.

Qualifying events include:

"I retired" absolutely counts as a life-changing event.

If you retire in 2024 and your income drops significantly, you can file Form SSA-44 to request a reduction in your 2026 IRMAA. You'll need documentation showing the life-changing event and your new expected income.

This is one area where being proactive pays off. Don't just accept the IRMAA bill when it arrives. If your circumstances changed, file the appeal. Social Security will reassess your premiums based on more current income information.

The key to managing IRMAA isn't avoiding it entirely—if you had a successful legal career, you're going to pay it in early retirement. Maybe throughout your entire retirement. But with some planning efforts, you may be able to minimize the amount you pay and/or the length of time that you’re subject to these additional payments.

Start planning at least three years before Medicare enrollment. Understand how your current financial decisions—Roth conversions, capital gains realization, business income—will affect your IRMAA two years later.

If you're retiring before 65, map out your income strategy for those gap years. This is when you have the most flexibility to control your taxable income and potentially execute larger Roth conversions before IRMAA becomes a factor.

Once you're on Medicare, review your IRMAA bracket annually. If you're close to a threshold, you might adjust that year's Roth conversion, capital gains harvesting, or other income-generating moves to stay below the next tier.

And remember to file Form SSA-44 promptly when you retire or experience another qualifying life event. Getting your IRMAA reduced based on current income rather than two-year-old earnings can save you thousands.

IRMAA can feel like a penalty, but it’s really not—it's means-testing. If you earned good income during your legal career, you'll pay more for Medicare. That's just how the system works.

But you don't have to accept whatever IRMAA bill arrives without question. With proper planning, you can coordinate your Roth conversions, manage your income strategically, and file appeals when circumstances change.

This is exactly why Medicare planning needs to be integrated with your overall retirement and tax strategy—not treated as a separate administrative task you handle on your own.

If you’d like more help on this topic, here are three options:

Financial Advisor

Financial planning & investment management services for families & businesses

📍405 E Chocolate Ave, Suite 101 A, Hershey, PA 17033

Serving clients virtually nationwide